Single Life Expectancy Table Irs 2017

Irs Proposes New Rmd Life Expectancy Tables To Begin In 2021 Life Expectancy Periodic Table Life

New Irs Announces 2018 Tax Rates Standard Deductions Exemption Amounts And More Standard Deduction Tax Brackets Tax Rate

How To Maximize Ira Accumulations

Impact Of The Proposed Irs Mortality Tables And Strategies To Reduce Its Effects Cammack Retirement Group Inc

Services Mcdonald Cech Financial Strategies Group Indianapolis In Wells Fargo Advisors

5 10 1 Pre Seizure Considerations Internal Revenue Service

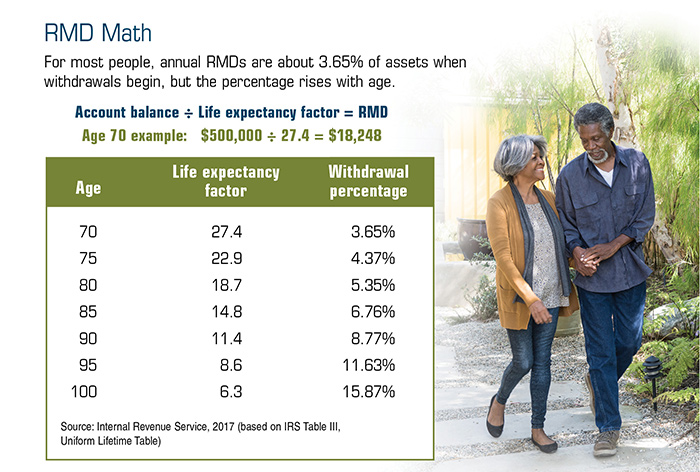

2016 life expectancy factor based on the irs single life expectancy table 21 0.

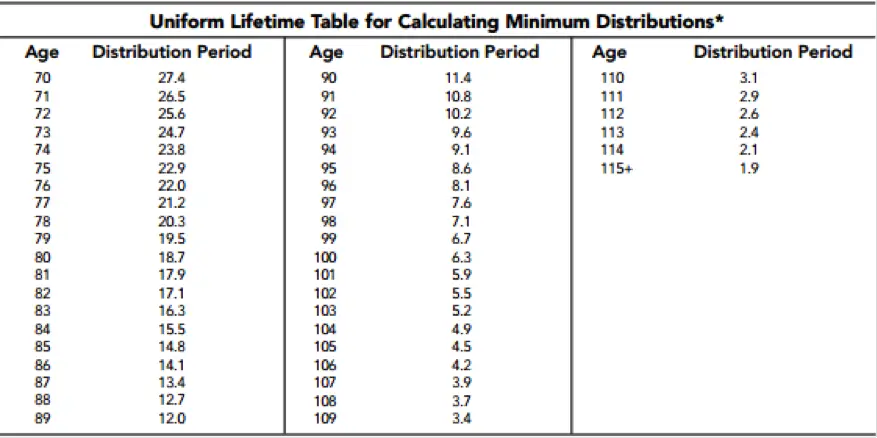

Single life expectancy table irs 2017.

Internal Revenue Bulletin 2017 26 Internal Revenue Service

Calculating The Required Minimum Distribution From Inherited Iras Morningstar

Be Aware Of Tsp Spousal Beneficiary Rules Fedsmith Com

How Changes In Retirement And Tax Law Will Help Save You Cash In 2020

Blank Invoice Templates Pdf Format Blank Invoice Template Pdf Why Downloading Blank Invoice Template Pdf Invoice Template Label Templates Receipt Template

Internal Revenue Bulletin 2020 29 Internal Revenue Service

Tax Deferred Exchanges Of Life Insurance Under Section 1035

Https Us Matthewsasia Com Resources Docs Pdf Literature Ira Application Current Pdf

Https Perkinsaccounting Com Wp Content Uploads 2018 Beyond Income Tax Returns Guide Pdf

Tsp Changes Required Minimum Distributions Rmds Federal Employee S Retirement Planning Guide

Http Www Jimhelps Com Wp Content Uploads 2013 07 Singlelifetable V 2 Pdf

Rmds And The Cares Act A Boon For Retirement Planners Bank Investment Consultant

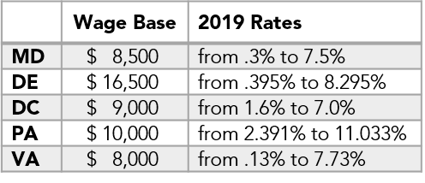

2019 Payroll Update

Https Www Tiaainstitute Org Sites Default Files Presentations 2017 06 Horneff 20maurer 20mitchell 20putting 20pension 20back 20in 20401k 20plans T 26i June2017 0 Pdf

Trends In The Internal Revenue Service S Funding And Enforcement Congressional Budget Office

Impact Of A Rapid Decline In Malaria Transmission On Antimalarial Igg Subclasses And Avidity Biorxiv

Https Www Governmentattic Org 37docs Irsqfr Cy2017 2020 Pdf

Life Expectancy Calculator Immediateannuities Com

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcrlncwuat Rs1 1iqs1liv7in4lxzll7lkualrxxhnifxdydqxx Usqp Cau

Irs1 Gene Genecards Irs1 Protein Irs1 Antibody

Lowered 2004 Dodge Ram 1500 Google Search Dodge Trucks Dodge Trucks Ram 2004 Dodge Ram 1500

Vvnwyoub5uns6m

Https Ljpr Com Wp Content Uploads 2015 07 Interest Rates And Lump Sums Approved Pdf

How To Keep The Inherited Iras From The Irs Retirement Watch

Source : pinterest.com